Financing a motorhome isn't quite like buying a car. You're securing a specialized recreational loan, and lenders are going to be looking closely at your credit score, income stability, and how much cash you can bring to the table. It all starts with a hard look at your own finances, building a real-world budget for ownership, and saving up a solid 10-20% down payment. Nail these, and you'll get the best possible loan terms.

Before you start walking through shiny new motorhomes and dreaming about your first big trip, the real work starts at your desk with a calculator. Laying a solid financial groundwork is the key to not only getting approved for a loan but getting one that won't become a burden down the road. Think of it as your pre-flight check before taking off into RV life.

Lenders tend to view motorhomes as luxury items. That means they'll scrutinize your financial health much more carefully than they would for a typical auto loan. How well you prepare now can be the difference between a smooth approval process and a frustrating dead end.

Your credit score is the first—and most important—thing a lender will look at. It's their quick snapshot of how reliable you are with debt. A strong score, usually 700 or above, is your ticket to the best interest rates and most favorable loan terms.

For example, a buyer with a 760 credit score might get an offer for a 6% interest rate. Someone with a 660 score applying for the same loan could be looking at 9% or even higher. On a 15-year loan, that difference can easily add up to tens of thousands of dollars in extra interest.

But it’s not just about that one number. Lenders will also dig into your full credit report, paying close attention to:

- Payment History: A clean record of on-time payments is a must-have.

- Debt-to-Income (DTI) Ratio: They want to see that your current debts aren't eating up too much of your monthly income.

- Credit Utilization: Keeping your credit card balances low shows you aren't overextended.

The sticker price is just the starting line. One of the biggest mistakes I see new buyers make is completely underestimating the true cost of owning a motorhome. Your budget has to go way beyond the monthly loan payment.

A realistic budget includes all the recurring expenses that can add hundreds of dollars to your monthly costs. To get a clear picture of what you can actually afford, you need to factor everything in. You can get a detailed breakdown by checking out our guide on how much an RV costs.

A motorhome isn't just a vehicle; it's a second home on wheels, and it comes with similar responsibilities. Forgetting to budget for maintenance, insurance, and storage is like buying a house and forgetting about property taxes and utilities.

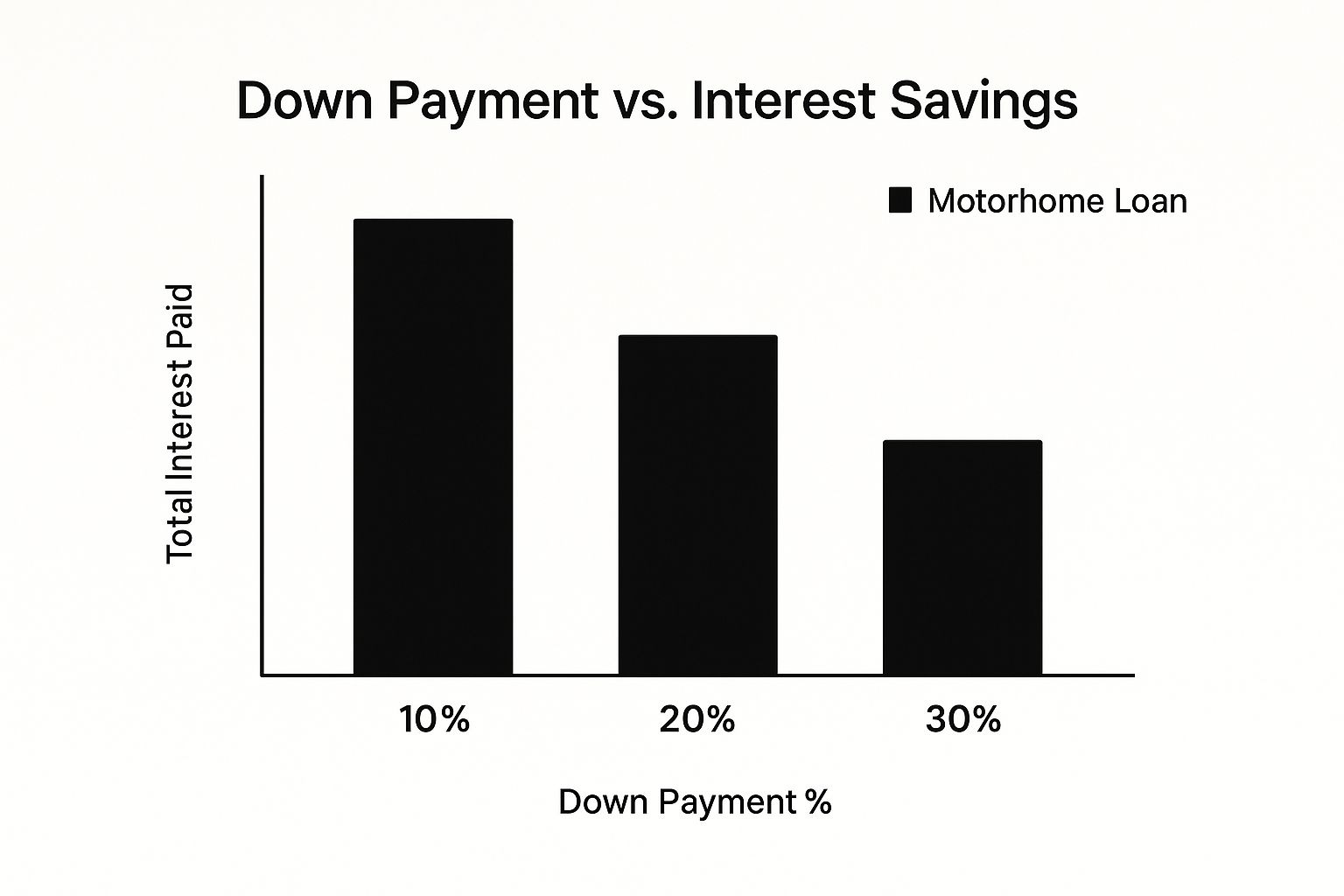

Your down payment is the most powerful tool you have for making a motorhome more affordable. Most lenders will want to see a minimum of 10% down, but if you can push that to 20% or more, you're in a much stronger position. A bigger down payment proves you're financially disciplined and lowers the lender's risk, which they'll often reward with a lower interest rate.

Buying a motorhome is a major financial decision. Prices can start around $50,000 for simpler models and soar past $200,000 for high-end Class A rigs. Because of this, most people need financing, and rates typically fall between 5% and 10%, depending heavily on credit. If you want to dig deeper, you can explore more data about the recreational vehicle financing market to see how these trends play out.

This chart shows just how much you can save in the long run by putting more money down upfront.

As you can see, that jump from a 10% to a 20% down payment has a huge impact on the total interest you'll pay, saving you thousands of dollars over the life of the loan.

Okay, you've done the hard work of getting your financial house in order. Now comes the exciting part: choosing where to actually get the loan. This decision is a bigger deal than most people realize.

The lender you choose will have a huge impact on your monthly payment, interest rate, and the total cost of your motorhome. Don't just settle for the first approval you get. A bit of smart shopping here can save you thousands over the life of your loan.

The Main Players in Motorhome Lending

When you start your search, you'll quickly find that most financing options fall into one of four buckets. Each one has its own vibe and its own pros and cons.

- Traditional Banks: Think of the big national and regional banks you see everywhere. They’re stable and predictable, but sometimes their RV loans feel like a slightly tweaked car loan, which might mean less flexible terms.

- Credit Unions: Since they're member-owned non-profits, credit unions often have a reputation for offering fantastic rates. Their goal is to serve their members, not shareholders, which can lead to better service and lower fees.

- Dealership Financing: This is the path of least resistance. You find your rig, and the dealer’s finance office handles the paperwork right there. It’s convenient, sure, but that ease can come with a price tag in the form of higher interest rates.

- Specialized RV Lenders: These companies are the pros. They only do recreational vehicle loans. They get that a motorhome is a long-term asset and are often willing to offer longer loan terms, sometimes up to 20 years.

Making the right choice means knowing what you’re getting into with each one. For a deeper dive, our guide on the top RV financing options for your dream RV can help you weigh these lenders against each other.

To make things easier, let's break down how these lenders stack up side-by-side. Seeing the differences in black and white can help clarify which route is the best fit for your situation.

| Financing Source |

Typical Interest Rate Range |

Common Loan Term |

Best For |

| Traditional Bank |

Moderate |

7-15 Years |

Borrowers with strong credit who value an established relationship and a streamlined digital process. |

| Credit Union |

Low to Moderate |

7-15 Years |

Members looking for the most competitive rates and personalized, community-focused service. |

| Dealership Financing |

Moderate to High |

10-20 Years |

Buyers who prioritize on-the-spot convenience and want the dealer to handle all the legwork. |

| Specialized RV Lender |

Moderate |

10-20+ Years |

Securing the longest possible loan terms, financing older or unique models, or for complex situations. |

As you can see, there's no single "best" option—it all comes down to what you prioritize. Do you want the absolute lowest rate, the most extended term, or the fastest approval? Your answer will point you in the right direction.

It's so easy to just say "yes" to the financing offered at the dealership. You've just spent hours finding the perfect motorhome, you're excited, and the finance manager can get it all done in less than an hour. That "one-stop-shop" model is powerful.

But you have to be careful. The dealership's finance office is a profit center. They work with a network of banks and often get a commission for sending them your loan. This can create an incentive for them to mark up the interest rate they offer you.

Pro Tip: Always walk into a dealership with a pre-approval from your bank, credit union, or an online lender. It's your ultimate bargaining chip. If the dealer can't beat the rate you already have, you can confidently walk away and use your backup plan.

Don't overlook the specialized online RV lenders. Companies like Essex Credit or LightStream live and breathe this stuff. They understand that a well-maintained motorhome holds its value far better than a car, and their loan products reflect that reality.

These lenders are often your best bet for getting financing on a slightly older used model or for securing those extra-long loan terms of 15 to 20 years, which can make a huge difference in your monthly payment. Their focused expertise often leads to a much smoother approval process because they know exactly what they're looking at.

The demand for these loans is booming. The RV financing market is expected to grow from USD 13.4 billion in 2024 to USD 20 billion by 2035. This isn't just a random statistic; it means the market is healthy and competitive, which is great news for you as a buyer. More competition means more pressure on lenders to offer you a great deal.

Applying for a loan that can easily stretch into six figures sounds like a big deal, and it is. But it doesn't have to be intimidating. With the right prep work, you can turn a potentially stressful experience into a smooth, straightforward process. This is the moment where all your financial groundwork pays off, giving you real buying power.

Ultimately, your goal is to prove one simple thing to the lender: you're a reliable borrower who can comfortably make the monthly payments. Every document you gather and every number on your application is part of that story. When you have everything ready to go, you don't just avoid delays—you present yourself as a serious, organized buyer.

The last thing you want is to be digging through file cabinets for old paperwork while the perfect motorhome—and a great deal—is on the line. Before you even think about filling out an application, take an hour to pull together your complete financial picture. I've seen this simple step shave days, sometimes even weeks, off the approval timeline.

Lenders need a clear view of your income, assets, and overall financial history. Here’s a quick checklist of what you’ll need to have ready:

- Proof of Income: This typically means your W-2s and tax returns from the past two years. If you're self-employed, plan on providing at least two years of business and personal tax returns, along with a recent profit and loss statement.

- Recent Pay Stubs: Grab your last two pay stubs to show your current income is stable.

- Bank and Investment Statements: Lenders want to see the last two or three months of statements for all your accounts—checking, savings, investment, you name it. This verifies you have the funds for a down payment and some cash reserves.

- Identification: A clear copy of your driver's license or another government-issued ID is a must.

- Proof of Residence: A recent utility bill or bank statement with your current address usually does the trick.

A pro tip? Scan and save these as PDFs in a dedicated folder on your computer. It makes filling out online applications a breeze.

Once your application is submitted, it lands on an underwriter's desk. This isn't just a computer algorithm; it's a real person whose job is to assess the risk of lending you a significant amount of money. They’re trained to look past the credit score and understand the full story behind your finances.

Their primary focus will be your Debt-to-Income (DTI) ratio. This is a simple calculation: your total monthly debt payments (including the potential new motorhome loan) divided by your gross monthly income. Most lenders want to see a DTI of 45% or lower.

Underwriters also comb through your bank statements looking for red flags like frequent overdrafts or large, undocumented cash deposits. They're trying to confirm your income is stable and you manage your money responsibly.

A clean, well-documented application sends a clear message to an underwriter: you're a low-risk borrower. Any missing information or inconsistencies will grind the process to a halt while they investigate every detail.

If there's one piece of advice I can give you on how to finance a motorhome, it’s this: get pre-approved for your loan before you start shopping seriously. A pre-approval isn't just a quick quote; it's a conditional commitment from a lender to give you a loan up to a specific amount, based on a full review of your financial documents.

Walking into a dealership with a pre-approval letter in hand completely flips the script. You're no longer just a "shopper"—you're a qualified buyer with cash in hand, figuratively speaking. This gives you enormous negotiating power. You can focus 100% on getting the best price for the motorhome because the financing is already sorted out.

It also acts as a built-in reality check, preventing you from falling in love with a rig you can't realistically afford. Your pre-approval sets a firm spending limit, keeping your search focused and your budget intact. It’s the single best way to buy with confidence from a position of strength.

https://www.youtube.com/embed/YbjGvgp19pM

Getting pre-approved for your motorhome loan is a huge step, but the work isn't quite done. Now it's time to focus on the fine print—the interest rate and the repayment term. These two factors will dictate your monthly payment and how much you ultimately pay for your rig over the next several years.

Even a small improvement here, like shaving half a percentage point off your interest rate, can save you thousands. This is where a little bit of strategy really pays off.

The recreational vehicle (RV) financing market is a big business, estimated to be worth around USD 39.58 billion by 2025. This means lenders are actively competing for customers just like you, which gives you more leverage than you might think. You just have to know how to use it. You can dig deeper into the RV financing market on MordorIntelligence.com.

Your credit score is the most powerful tool in your negotiation toolkit. To a lender, a high score signals that you're a low-risk borrower, which is exactly who they want to offer their best rates to.

If you have a strong score (think 740+), don't hesitate to use it. When you see their offer, you can simply ask, "Is this the best possible rate for someone with my credit profile?" It's a polite way of nudging them to give you their top-tier pricing.

But the single most effective tactic is to have multiple offers in hand. Never just accept the first approval you get. Make a point to apply with at least three different lenders—try a local credit union, a major national bank, and a lender that specializes in RVs.

Once the pre-approvals start rolling in, you can strategically play them off one another. For instance, if Lender A offers you 7.5% but Lender B comes in at 7.2%, circle back to Lender A. You could say something like, "I really appreciate the offer and would prefer to work with you, but I have another approval at 7.2%. Can you get closer to that number?" More often than not, they'll find a way to sweeten the deal.

Motorhome loans are a bit unique because they can have incredibly long repayment periods—it’s not uncommon to see terms of 10, 15, or even 20 years. The obvious benefit of a longer term is a lower, more comfortable monthly payment, which can be very tempting.

But be careful. That lower monthly payment comes at a significant cost. The longer your loan term, the more you'll pay in total interest.

It's easy to get fixated on the monthly payment, but you have to look at the total cost of borrowing. A slightly lower payment today could easily cost you tens of thousands of extra dollars over the life of the loan.

To really see this in action, it helps to play with the numbers. You can see how different terms will impact your own situation by plugging some numbers into our interactive RV loan calculator.

Let’s run through a quick example. Imagine you’re financing $100,000 at a 7% interest rate. Here’s how the term changes everything:

| Loan Term |

Monthly Payment |

Total Interest Paid |

| 10 Years |

$1,161 |

$39,329 |

| 15 Years |

$899 |

$61,794 |

| 20 Years |

$775 |

$86,071 |

Look at that difference. Stretching the loan from 10 to 20 years lowers your payment by nearly $400 a month, but it will cost you an extra $46,742 in interest. The best advice is to choose the shortest loan term you can comfortably fit into your budget.

When you’re finally sitting down with the dealership’s finance manager, remember that almost everything on the table is negotiable. It’s not just about the interest rate.

Be ready to discuss a few other key items:

- Loan Fees: Ask for an itemized list of all fees. Are there application or origination fees? It never hurts to politely ask if any of them can be reduced or waived entirely.

- Prepayment Penalties: This is a big one. Make absolutely sure the loan has no penalty for paying it off early. You always want the freedom to pay down your principal faster without getting hit with extra charges.

- Add-Ons and Warranties: The finance manager will almost certainly offer you extras like extended warranties, GAP insurance, or tire protection plans. While some of these can have value, they also get rolled into your loan, increasing your total debt. Analyze each one carefully and don't feel pressured to accept anything you don't need.

Walking into that final meeting with confidence and a solid grasp of the numbers is how you turn a good deal into a great one. This final step ensures your new motorhome is purely a source of adventure, not a financial burden.

You’ve found the perfect motorhome. The excitement is building. Now you’re in the final stretch—the financing—and it’s tempting to rush through the paperwork just to get the keys in your hand. But this is exactly where some of the costliest mistakes are made.

Slowing down right now is the single best thing you can do to protect your investment. I’ve seen countless buyers, swept up in the moment, fall into simple traps that tack thousands of extra dollars onto their loans. Let’s walk through the big ones so you can spot them a mile away.

The first thing most people want to know is, "What's my monthly payment?" Finance managers at dealerships are experts at using this to their advantage. They'll often present a loan offer with a beautifully low monthly number that seems too good to pass up.

Here's the catch: that low payment is almost always achieved by stretching the loan out over an incredibly long term, sometimes 15 or even 20 years. As we've covered, this massively inflates the total interest you pay. Don't fall for it. Your question shouldn't just be about the monthly payment; it should be, "What is the total cost of this loan?"

If you’re trading in a vehicle you still owe money on, you might be dealing with negative equity. This just means you owe more on the loan than the vehicle is actually worth. A common tactic is for a dealer to offer to "make that debt disappear" by rolling it into your new motorhome loan.

This is a financial sinkhole. Let's say you're $5,000 "upside down" on your trade. That $5,000 doesn't vanish—it gets tacked onto the principal of your new loan. Now you’re paying interest on that old debt for the next two decades, and you're starting off owing far more than your brand-new motorhome is worth.

The best way to handle negative equity is to pay it off separately if you possibly can. Rolling it into a new long-term loan is like chaining an anchor to your rig before you even drive it off the lot.

Loan agreements are notoriously long and boring, but the devil is truly in the details. You need to be a detective and hunt for two specific things: junk fees and prepayment penalties.

- Junk Fees: Scan the contract for vague charges. Things like "dealer prep fees," "loan processing fees," or "documentation fees" can be legitimate, but they're also often inflated for pure profit. Question every single line item you don't understand. Ask for it to be explained, and if the explanation is flimsy, ask for it to be removed.

- Prepayment Penalties: This is a nasty little clause that slaps you with a fee if you decide to pay your loan off early. You absolutely want the freedom to make extra payments or pay off the whole thing ahead of schedule without getting penalized. Make sure your contract explicitly states there is no prepayment penalty.

Once you're in the finance office, you’ll likely be presented with a whole menu of optional products. These range from extended warranties and GAP insurance to pricey tire protection plans and fabric sealant. While some of these might have value, they are also massive profit centers for the dealership.

Every add-on you agree to gets rolled into your loan amount. This not only increases your monthly payment but also the total interest you’ll pay over the long haul. My advice? Politely decline everything at first. If an extended warranty sounds appealing, go home and research third-party options. They are frequently cheaper and offer better coverage. Never let anyone pressure you into making a snap decision on these expensive extras.

Once you start seriously shopping, the big-picture questions get replaced by much more specific ones. That’s a good sign—it means you're getting close. Nailing down these details is what separates a smooth financing experience from one with unwelcome surprises.

Let's walk through some of the most common questions we hear from people just like you. Getting these answers straight will give you the confidence to make your final decision.

Yes, absolutely. Financing a used motorhome is not only possible, it's often a brilliant financial move. The process isn't all that different from financing a new one, but you should expect lenders to have a few extra requirements.

For instance, many lenders put an age cap on the vehicles they'll finance—often nothing older than 10 years. They might also have mileage limits. You'll likely see a slightly higher interest rate compared to a brand-new model, which is the lender's way of balancing out the perceived risk.

But don't let that deter you. The significantly lower purchase price of a pre-owned rig can easily outweigh a slightly higher rate. The one thing you can't skip? A professional, independent inspection. The last thing you want is to finance someone else's hidden problems.

This is one area where RV loans are a world away from a standard auto loan. Because motorhomes are a major purchase, the loan terms are stretched out to make them more affordable. It's completely standard to see financing that runs from 10 to 15 years.

On the higher-end, six-figure coaches, some specialized lenders will even offer terms as long as 20 years.

A longer term can be a bit of a trap. Sure, it gets you that lower, more comfortable monthly payment, but it also means you'll pay a whole lot more in interest over the life of the loan. My advice is always to take the shortest term you can genuinely afford.

This is the big one, and the answer is a potential "yes." The IRS has specific rules, but if your motorhome has sleeping, cooking, and bathroom facilities, it can often be classified as a second home.

If your rig qualifies, the interest you pay on the loan could become tax-deductible, just like the mortgage interest on a stationary house. That can be a huge financial perk over the years.

But tax laws are notoriously tricky and they change. This isn't something to figure out on your own. It's crucial to talk to a qualified tax professional who can look at your specific situation and tell you definitively if you're eligible for this deduction. Don't leave this to chance.

You'll want to aim for a down payment between 10% and 20% of the purchase price. That's the industry standard for a reason. While you might see lenders offering deals with little to no money down, putting more skin in the game is always the smarter long-term play.

A solid down payment does a few really important things for you:

- You borrow less money. Simple, but powerful.

- Your monthly payment will be lower. A smaller loan means a smaller payment.

- You look better to lenders. A good down payment improves your loan-to-value (LTV) ratio, making you a less risky borrower and helping you score a better rate.

- You start with equity. You’ll owe less than the motorhome is worth from the get-go, which protects you from the steep depreciation that happens the second you drive off the lot.

Think of it this way: a strong down payment is the best way to make your life on the road more affordable from day one.

Ready to turn your travel dreams into reality? At Searchshop, we simplify the process of finding and financing your perfect motorhome. Explore our extensive inventory and discover financing tools to get you on the road faster.