Financing an RV is more than just picking a model and signing on the dotted line. It’s about securing a loan that fits your budget, and that process starts long before you step onto a dealer's lot. The smart way to approach it is to first check your credit, figure out exactly what you can realistically afford, and then shop around for the best loan terms. Only then should you start looking for your perfect RV.

Your Financial Roadmap to RV Ownership

The dream of hitting the open road in your own RV is a powerful one, but it starts with a solid financial plan, not just wanderlust. Understanding how to finance an RV is the critical first step. Think of it as mapping out your route before you start driving; it helps you navigate the process, avoid wrong turns, and reach your goal without any expensive surprises.

This isn't just about getting a loan—it's about making a series of smart decisions that will impact your finances for years. And you're not alone in this journey. The global Recreational Vehicle financing market was valued at around $36.75 billion in 2025 and is on a steady climb, fueled by a growing desire for travel freedom. You can learn more about these market trends and their drivers. More interest means more financing options for you, but it also makes doing your homework even more important.

The Core Components of RV Financing

Before you start filling out loan applications, you need to get a handle on the three main pieces of the financing puzzle. Each one plays a huge role in whether you get approved and, more importantly, what kind of loan you'll get. They all work together, and improving one can often give the others a boost.

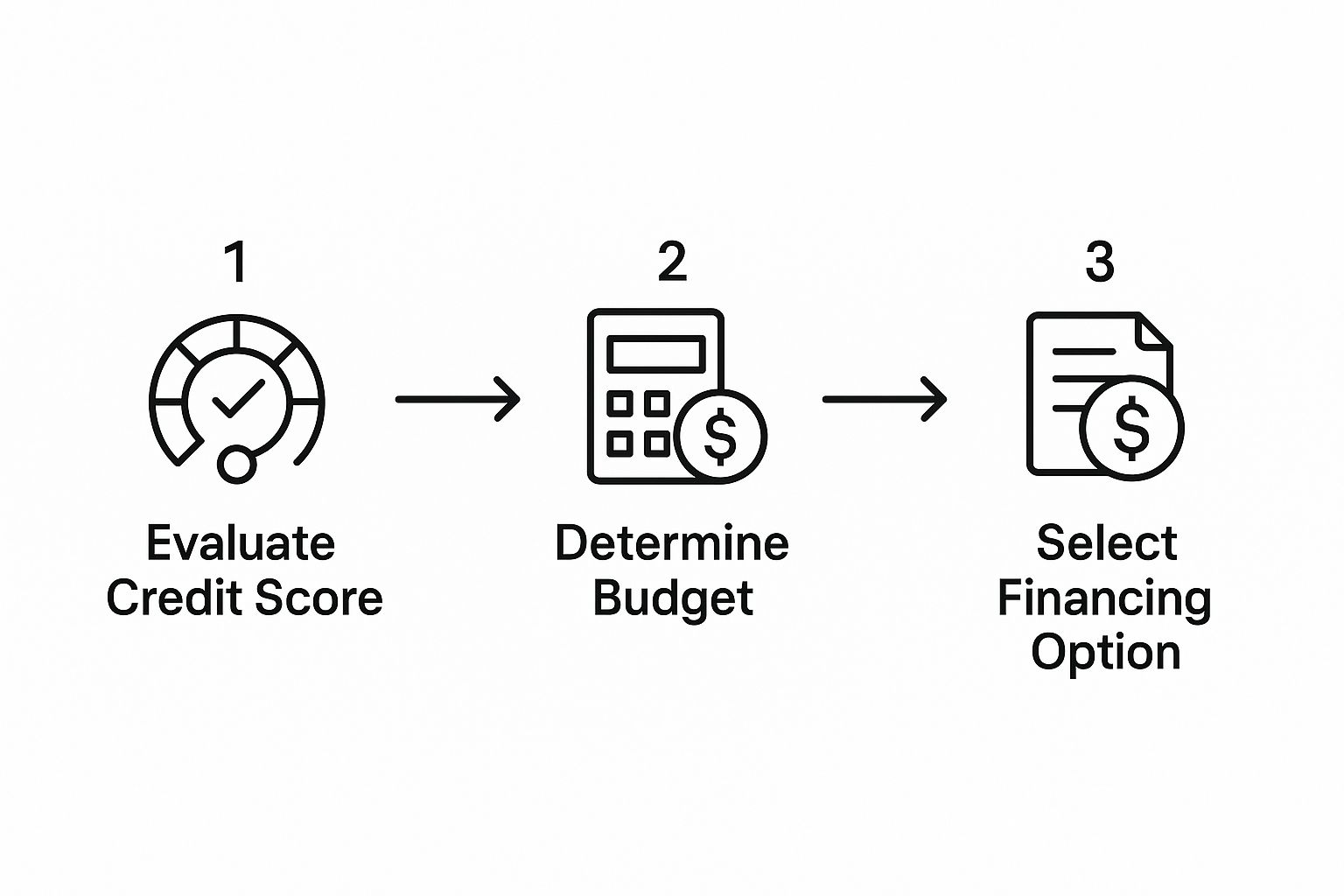

The infographic below breaks down where the journey really begins.

As you can see, it all starts with a financial self-check. This is the non-negotiable first move you need to make before ever talking to a lender.

Your financing journey kicks off with an honest look at your own situation. These initial steps are like a pre-flight checklist, making sure you're ready for the conversations ahead.

-

Credit Score Evaluation: Think of this three-digit number as your financial passport. Lenders use it as the main yardstick to measure how reliable you are as a borrower. A higher score will almost always unlock lower interest rates and better terms, which can save you thousands over the life of the loan.

-

Budget and Affordability: This is about more than just the price tag on the RV. A real-world budget has to include the monthly payment, insurance, maintenance, storage fees, and fuel. Understanding this total cost of ownership keeps you from buying an RV you can afford to purchase but not actually use.

-

Lender Options: Don't assume the dealership is your only option. The main players are traditional banks, credit unions (which are often great for members), and the dealership's in-house financing department. Each has its own pros and cons, from a credit union's competitive rates to a dealer's convenience.

The single best move you can make is to walk into a dealership with a pre-approval letter from your own bank or credit union. It completely changes the conversation. You’re no longer just applying for a loan; you’re a cash buyer in their eyes, and that gives you all the negotiating power.

To give you a clearer picture, here's a breakdown of the key stages you'll go through.

Key Stages of RV Financing

This table walks you through the essential steps in the RV financing process, from doing your homework at the kitchen table to finally getting the keys.

|

Financing Stage |

What You Need to Do |

Why It Matters for Your Loan |

|---|---|---|

|

1. Self-Assessment |

Check your credit score and review your credit report for errors. |

A higher score means better loan offers. Fixing mistakes can boost your score quickly. |

|

2. Budgeting |

Calculate a realistic monthly payment, including insurance, fuel, and maintenance. |

This prevents you from over-borrowing and ensures you can truly afford the RV lifestyle. |

|

3. Pre-Approval |

Apply for a loan with a bank or credit union before you shop. |

Gives you a firm budget and massive leverage when negotiating price with the dealer. |

|

4. RV Shopping |

Find the RV that fits your needs and your pre-approved budget. |

You can shop with confidence, knowing exactly what you can spend without financial strain. |

|

5. Finalizing the Loan |

Compare the dealer's financing offer against your pre-approval and choose the best one. |

A little comparison shopping here can save you hundreds or even thousands in interest. |

Following these stages in order puts you in control and helps you make a sound financial decision for the long haul.

Preparing for a Successful Application

Once you've got these concepts down, it's time to get your paperwork in order. This preparation phase is all about positioning yourself as a low-risk, ideal candidate for a loan. Lenders want to see stability and a track record of managing debt well.

Go ahead and gather your key financial documents now. This usually means your last two years of tax returns, recent pay stubs, and a couple of months' worth of bank statements. Having everything ready to go shows lenders you're serious and organized, making the whole application process smoother and faster. This simple prep work sets the stage for a confident financing experience and gets you that much closer to hitting the open road.

Finding the Right RV Loan for Your Rig

Not all RV loans are cut from the same cloth. Honestly, picking the right financing can save you thousands over the years—it's just as crucial as choosing the perfect floor plan. The loan you sign on for will dictate your monthly payment, how much interest you ultimately pay, and your overall financial wiggle room.

For most people, the go-to option is a secured loan. It’s pretty straightforward: the RV itself is the collateral. This just means that if you can't make the payments, the lender can repossess the RV to recoup their money.

Because the lender has that safety net, they're usually willing to offer better interest rates and longer repayment periods. This is the most common path you'll see when you start looking into how to finance an RV.

RV Loans Aren't Just Big Car Loans

It’s easy to think an RV loan is just a supersized auto loan, but there are some key differences. The biggest one? The loan term—how long you have to pay it back. A typical car loan might run for five to seven years, but RV loans often go much, much longer.

It’s not at all strange to see specialized RV loans with terms stretching from 10 to 20 years. That longer timeline is what makes the monthly payment on a big-ticket purchase feel manageable. But here's the catch: a longer term means you'll pay a lot more in total interest.

Let’s run some numbers. Say you get a $75,000 RV loan at an 8% interest rate.

-

On a 10-year term, your monthly payment would be about $910.

-

Stretch that to a 15-year term, and the payment drops to around $717.

That sounds great, right? But the total interest paid skyrockets from $34,150 to $54,100. It’s a classic trade-off between a lower monthly bill and the long-term cost.

Secured vs. Unsecured Loans

Beyond the typical loans from banks and dealers, there’s also the unsecured personal loan. Unlike a secured loan, this one isn't tied to an asset. You're borrowing based purely on your creditworthiness.

Here’s a quick breakdown of how they stack up:

|

Loan Feature |

Secured RV Loan |

Unsecured Personal Loan |

|---|---|---|

|

Collateral |

The RV itself |

None required |

|

Interest Rates |

Generally lower Shop RVs For SaleBrowse current rvs from dealers near you — updated daily. |

Typically higher |

|

Loan Amounts |

Can be very large |

Usually smaller limits |

|

Lender Risk |

Lower for the lender |

Higher for the lender |

Unsecured loans aren't the first choice for buying a whole RV. Their borrowing limits are usually lower, and the interest rates are higher because the lender is taking on all the risk. Still, an unsecured loan could be a perfect fit for a smaller, used camper or for financing a big renovation on an RV you already own.

The Big Debate: Fixed-Rate vs. Variable-Rate

One of the most important decisions you'll face is choosing between a fixed-rate and a variable-rate loan. This choice directly impacts how predictable your monthly payments will be.

-

Fixed-Rate Loans: Your interest rate is locked in for the life of the loan. Your payment won't change, which makes budgeting a breeze. This is what most RV buyers go for because it offers peace of mind.

-

Variable-Rate Loans: The interest rate can change over time, as it's tied to a market index. It might start lower than a fixed rate, but if market rates climb, so will your monthly payment.

For a long-term purchase like an RV, a fixed rate is almost always the safer bet. It protects you from surprise payment hikes and lets you focus on planning trips, not stressing about interest rate news.

Banks and Credit Unions: The Power of Pre-Approval

Walking onto an RV lot with a pre-approval letter from your bank or credit union changes everything. Suddenly, you’re not just another person hoping for a loan; in the dealer's eyes, you're a cash buyer. This gives you a massive advantage when negotiating the price of the RV itself, not just the financing terms.

Here’s why this strategy is so effective:

-

You Know Your Limits: A pre-approval sets a hard ceiling on what you can spend. It keeps you grounded and prevents you from falling in love with a rig you can't realistically afford.

-

You Can Focus on the RV Price: With the loan part handled, your negotiation can be laser-focused on one thing: the price of the vehicle. You don't get sidetracked by confusing "low monthly payment" sales pitches.

-

You Have a Rate to Beat: You can confidently sit down with the finance manager and say, "Here's the rate my credit union gave me. Can you beat it?" If they can, you get an even better deal. If not, you've got your own loan ready to go.

Credit unions are often a goldmine for RV loans. Because they're not-for-profit and owned by their members, they're known for offering better rates and more flexible terms than many big banks.

Pro Tip: Always, always get at least one pre-approval from an outside lender before you start shopping for an RV. It is the single best tool you have for making sure you get a competitive rate.

A Real-World Example

Let's say a couple, Sarah and Tom, has their eye on a travel trailer with a $60,000 price tag. Before they even step into a dealership, they visit their local credit union. They get pre-approved for the full amount at a 7.5% interest rate over 12 years.

With that approval in hand, they find the perfect trailer and negotiate the price. When they sit down with the finance manager, he offers them a loan package at 8.25%.

Sarah and Tom simply show him their pre-approval letter. Lo and behold, the manager is suddenly able to find a lender who can match their credit union's 7.5% rate.

Just by doing a little prep work, they put themselves in the driver's seat and saved a significant amount of money over the life of the loan. Online lenders are also a great third option to check, as they can be very competitive and offer a fast application process.

Mastering Your Down Payment and Interest Rate

When you're figuring out how to finance an RV, two things matter more than almost anything else: your down payment and your interest rate. Getting these right won't just nudge your monthly payment down—it can save you thousands upon thousands of dollars over the life of the loan. Think of them as the two most powerful levers you can pull to make your dream RV truly affordable.

More people are pulling these levers than ever before. The global RV financing market swelled to around $35.7 billion by 2024, and it's not slowing down. This isn't just a number; it reflects a massive cultural shift toward lifestyles built on freedom, remote work, and outdoor adventure. You can get a deeper look into the trends shaping RV financing and see what's driving this growth.

The Power of a Strong Down Payment

One of the first questions I always hear from buyers is, "How much do I really need to put down?" You'll see some lenders dangling zero-down offers, but the sweet spot—and the industry standard—is typically between 10% and 20% of the RV's total price.

Putting down a good chunk of cash is a strategic move. It shows lenders you’re a serious, lower-risk borrower, which often convinces them to give you a better interest rate. But there's a more important reason: it's your best defense against depreciation. RVs lose value the second they drive off the lot, and a solid down payment helps you avoid ending up "upside down"—a situation where you owe more on the loan than the RV is actually worth.

Being upside down is a financial trap. It makes selling or trading in your RV a nightmare, as you’d have to pay the lender the difference out of your own pocket. A 20% down payment is the gold standard for sidestepping this headache.

To put it in perspective, on a $70,000 travel trailer, a 10% down payment is $7,000. Bumping that up to 20% means you’ll need $14,000. That extra $7,000 upfront can completely change your loan terms for the better.

Decoding Your Interest Rate

Your interest rate is simply the cost of borrowing money. Over a long RV loan, even a tiny difference in that rate can have a massive impact on your total cost. Lenders don't just pull these numbers from a hat; they’re calculated based on a risk assessment of you and the RV.

Several key factors come into play:

-

Credit Score: This is the big one. A higher score proves you have a history of paying your debts and almost always unlocks the lowest rates.

-

Loan Term: Longer terms, like 15 or 20 years, are common for RVs but often come with slightly higher interest rates. The lender is taking on risk for a longer period.

-

RV Age and Type: Lenders view a brand-new, high-end motorhome differently than a five-year-old pop-up camper. They often offer more attractive rates on newer models.

-

Your Down Payment: As we've covered, bringing more cash to the table reduces the lender's risk. They often reward you for this with a lower interest rate.

How Down Payments and Interest Rates Impact Your Loan

Let's look at some real numbers to see how these two factors work together. The table below illustrates how different scenarios can dramatically change your monthly payment and the total interest you'll pay on a hypothetical $70,000 RV loan with a 15-year (180-month) term.

|

Loan Details |

Down Payment |

Interest Rate |

Monthly Payment |

Total Interest Paid |

|---|---|---|---|---|

|

Scenario 1: Strongest |

$14,000 (20%) |

7.5% |

$518 |

$37,240 |

|

Scenario 2: Good |

$14,000 (20%) |

9.5% |

$585 |

$49,300 |

|

Scenario 3: Weaker |

$7,000 (10%) |

8.0% |

$602 |

$45,360 |

|

Scenario 4: Weakest |

$7,000 (10%) |

10.0% |

$677 |

$58,860 |

The difference is staggering. Pairing a strong 20% down payment with an excellent interest rate (Scenario 1) gets you a $518 monthly payment. In the weakest scenario, your payment jumps to $677—that's $159 more every single month.

Over the entire 15-year loan, the best-case scenario saves you a whopping $21,620 in interest compared to the worst-case. This is precisely why getting your credit score in shape and saving for a healthy down payment before you start shopping is the smartest way to finance an RV.

Navigating the Loan Application and Approval Process

You’ve done the hard work of researching, budgeting, and maybe even secured a pre-approval. Now comes the main event: the formal loan application. This is where all your preparation truly pays off, transforming what can feel like an intimidating step into a smooth path toward grabbing those keys.

Think of your application as the complete story of your financial health. Lenders are looking for a clear, consistent picture that proves you can handle the monthly payments for the life of the loan. Getting organized now can make all the difference in how quickly you get approved.

The North American market is a powerhouse in this industry, pulling in about 61.4% of global RV financing revenue in 2024. This is mostly thanks to a well-established dealership network and solid consumer credit laws that foster a competitive buying environment. You can dig into more details about the regional RV financing market here. For you, this means lenders are actively competing for your business, so a polished application helps you stand out.

Assembling Your Application Toolkit

Before you even think about filling out a form, get your documents in order. Having everything on hand shows lenders you’re serious and organized, which can make a surprisingly good impression. There's nothing worse than scrambling to find a pay stub or tax return at the last minute—it just adds stress you don't need.

Your lender will almost certainly ask for these items:

-

Proof of Income: Typically, this means your most recent pay stubs covering a 30-day period. If you're self-employed, be ready with at least two years of tax returns.

-

Identification: A valid, government-issued photo ID, like your driver's license, is a must.

-

Bank Statements: Lenders usually want to see the last two to three months of statements for your main checking and savings accounts.

-

Proof of Residence: A recent utility bill or bank statement showing your current address will do the trick.

A common hang-up I've seen is explaining bumps in a financial history. If you recently switched jobs or had a significant gap in employment, go ahead and draft a brief, honest letter of explanation. Addressing it upfront shows you're transparent and stops the lender from making their own assumptions.

Presenting Your Financial Story

Your application is more than just a pile of numbers; it’s your chance to present yourself as a reliable borrower. If you know there are potential dings on your credit report, like a late payment from last year, don't try to sweep them under the rug. Be prepared to explain what happened calmly and honestly if it comes up.

A simple, direct statement like, "I see that late payment from last March; that was right after I had a hospital stay, and all my accounts have been current since," can work wonders. It shows you take responsibility and frames the issue as a one-time event, not a habit. This kind of proactive communication is a huge part of learning how to finance an RV the right way.

What Happens After You Click Submit

Once your application is in, the lender's underwriting team takes over. This part of the process can feel like a mysterious black box, but it's actually a pretty straightforward review.

Here's a breakdown of what you can expect:

-

Initial Review: First, an automated system or a loan officer will check your application for completeness and pull your credit report.

-

Verification Calls: Don't be surprised if the lender calls your employer to confirm your job and income. This is a standard step to prevent fraud.

-

Conditional Approval: You might get a "conditional" approval, which means the loan is a go as long as you provide a few more documents or meet specific last-minute requirements.

-

Formal Offer: After everything checks out, you'll receive the formal loan offer. This is a legally binding document, so read it carefully. Make sure the interest rate, loan term, monthly payment, and total finance charge all match what you were quoted.

One of the biggest mistakes people make is shotgunning applications to a dozen different lenders. Every application triggers a "hard inquiry" on your credit report, and too many at once can ding your score. Stick to two or three lenders to compare offers without doing any damage. Signing that final loan agreement is the last hurdle, so take your time, ask every question you have, and make sure you understand every single line.

Tying Up the Loose Ends: Your RV Financing Questions Answered

Even with a solid financial plan, a few questions always seem to pop up right at the end. That's completely normal. Getting these last few details sorted out is the final step to feeling confident and ready to sign on the dotted line, ensuring there are no surprises down the road.

Let's tackle some of the most common "what-ifs" and "how-does-this-work" scenarios that I see come up all the time.

Can I Finance an Older or Used RV?

You bet. Financing a used RV is not only possible, it's often a really smart move. You let the first owner take the biggest hit on depreciation, which can save you a bundle. Lenders are perfectly comfortable with used models, but they do have a few ground rules.

Most will have some kind of age and mileage cutoff. For instance, a lender might draw the line at an RV that’s more than 10-12 years old or has a ton of miles on the clock. You may also find that the loan terms are a bit shorter for used rigs—think a 10-year term instead of a 15-year one for a brand-new model.

The good news is that the market is adapting. We're seeing more peer-to-peer RV lending platforms and online lenders who are making it easier to find financing for pre-owned models. These newer options often lead to quicker approvals and more transparent pricing, which is great for anyone shopping in the used market. You can dig deeper into global trends in recreational vehicle financing to see how things are evolving.

Are There Penalties for Paying Off My RV Loan Early?

This is a fantastic question to ask, and the answer can save you a serious amount of money. What you're looking for in the loan agreement is a clause about a prepayment penalty. Some lenders, especially those who work with buyers with lower credit scores, might charge you a fee if you pay off the loan ahead of schedule.

Why would they do that? Simple: lenders make their money on the interest you pay over time. If you pay it off early, they lose out on that projected income. The penalty is just their way of getting some of it back.

Before you sign anything, ask the lender point-blank: "Is there a prepayment penalty on this loan?" Most reputable banks and credit unions don't have them, but it’s a critical detail you absolutely must confirm.

Can I Get an RV Loan with Bad Credit?

It's definitely tougher to get an RV loan with a spotty credit history, but it's not impossible. You'll just find that your options are a bit more limited, and you should brace yourself for higher interest rates and a larger down payment requirement. From a lender's perspective, a low credit score signals higher risk, and they adjust the loan terms to protect themselves.

If you find yourself in this situation, here are a few things that can help:

-

Bring more cash to the table. A down payment of 25-30% can make a huge difference in your approval odds.

-

Find a co-signer. Partnering with someone who has excellent credit can help you secure a loan and get a much better rate.

-

Check with credit unions. They’re often more flexible and willing to look at your whole financial story, not just a three-digit score.

-

Go for an older, less expensive model. A smaller loan amount is less risky for the lender, which makes it easier to get approved.

Does RV Insurance Work Like Car Insurance?

It’s similar, but RV insurance is its own unique beast. Your lender will require you to have it, but you’ll want it for your own peace of mind anyway. Think of it as a hybrid policy that pulls elements from both auto and homeowners insurance.

An RV policy includes critical coverages you just won't find on a s