So, you’re ready to hit the open road. But before you start mapping out your national park tour, there's one crucial step: figuring out how to pay for your home on wheels.

The most common ways to finance an RV are through traditional bank loans, credit union loans, specialized RV lenders, and dealer financing. It helps to think of this process less like buying a car and more like getting a mortgage for a second home—the loan terms are longer, and the amounts are often much larger.

That dream of freedom and adventure is within reach, but the first stop on your journey isn't the dealership—it's understanding your financing. Getting a loan for an RV is its own unique ballgame. We’re talking longer repayment schedules, bigger loan amounts, and a financial commitment that deserves careful thought.

This guide is designed to be your compass, helping you navigate the world of RV loans with confidence. We’ll break down every path you can take, so you can make a smart, affordable choice that gets you behind the wheel and on your way.

The surge in RV popularity has created a massive financial market to support it. The global Recreational Vehicle (RV) financing market is currently valued at around $36.75 billion, and it's growing fast. That growth is being driven by more and more people wanting to explore the great outdoors. You can dig deeper into the RV financing market trends to see just how big this industry has become.

For you, this means more competition among lenders and plenty of options. But it also means you need to have a game plan.

Think of your RV loan as the foundation of your future travels. A strong, well-chosen financial plan ensures your adventures are built on stability, not stress. It allows you to focus on the memories you'll make, not the payments you owe.

Before we jump into specific lenders, let's cover a few core ideas that will pop up again and again. Getting a handle on these will make everything else much clearer.

We’ll explore:

- Secured vs. Unsecured Loans: We'll look at why using your RV as collateral can dramatically change your interest rates and terms.

- Loan Terms and Amortization: You'll see how repayment periods, often stretching from 10 to 20 years, impact both your monthly payment and the total interest you'll pay over time.

- Credit Score Impact: This is a big one. We’ll explain why your credit history is the single most important piece of the puzzle for any lender.

With this knowledge in your back pocket, you’ll be ready to compare the different rv financing options and find the one that truly fits your journey.

Before we dive into where to get your RV financing, we need to talk about the two fundamental ways these loans are structured. This is your first big decision, and it’s a crucial one. It sets the stage for everything that follows—your interest rate, how long you have to pay, and the amount of risk involved for both you and the lender.

Think of it like this: are you tying your loan directly to the RV, or are you getting a loan based on your financial reputation alone?

Almost every RV loan you'll come across is a secured loan. If you’ve ever financed a car or bought a house, this will feel very familiar. With a secured loan, the RV itself serves as collateral.

What does that mean? It’s simple: if you stop making payments, the lender has the legal right to take the RV back to get their money back.

This setup gives the lender a safety net, and that security gets passed on to you in the form of better terms. Because their risk is much lower, they're willing to offer:

- Lower interest rates than you’d get otherwise.

- Longer repayment terms, often stretching out 10 to 20 years, which keeps your monthly payments manageable.

- Higher loan amounts, making it possible to finance that dream Class A motorhome.

On the flip side, you have the unsecured loan, which is usually just a personal loan. This type of loan isn't tied to any physical asset. Instead, it’s approved based entirely on your personal creditworthiness—your credit score, income, and overall financial track record.

The biggest plus here is flexibility. You can sometimes use the money for more than just the RV, and the approval process is often quicker because there's no vehicle to value. But that convenience comes with a price tag.

An unsecured loan is purely a bet on your promise to pay it back. The lender has no collateral to fall back on if you default, so they're taking on all the risk. That risk is always baked into the cost of the loan.

Since the lender is taking a much bigger gamble, unsecured loans almost always have higher interest rates and much shorter repayment periods. This makes them a more expensive and less common way to finance a major purchase like an RV. For the vast majority of buyers, the superior terms of a secured loan make it the obvious and more practical choice among the various RV financing options out there.

When you start thinking about how to pay for your dream RV, the most natural place to start is with the financial institutions you already know and trust. This is a smart move. Both national banks and your local credit union are well-versed in handling these kinds of large recreational loans.

Think of it this way: these lenders often treat an RV loan like a mortgage for a second home. It's a significant asset and a long-term commitment. Because of this, their application process is going to be pretty thorough to make sure you can comfortably handle the payments for years to come.

Before you even fall in love with a specific Class A or travel trailer, it's a good idea to get your financial house in order. When you apply for a loan, lenders will zero in on a few key things to figure out if you're a good risk and what kind of loan terms they can offer.

Here’s what they’ll be looking at under a microscope:

- Credit Score: This is the big one. To get the best interest rates and most favorable terms, you’ll want a credit score of 700 or higher.

- Debt-to-Income (DTI) Ratio: Lenders want to see that your existing monthly debt payments aren't eating up too much of your income. They need to be confident you can add an RV payment without stretching yourself too thin.

- Down Payment: Putting more money down reduces the lender's risk, which they love. Be prepared to put down at least 10-20% of the purchase price. A bigger down payment not only helps you borrow less but often unlocks a lower interest rate.

Here's a pro tip: Get pre-approved before you start shopping. Walking into a dealership with a pre-approval letter is a huge advantage. It proves you're a serious buyer and gives you a firm budget to stick to.

While banks and credit unions both offer RV loans, they come at it from different angles. Knowing how they operate can save you real money.

A traditional bank often rewards loyalty. If you already have a mortgage, checking account, or investments with them, you might get a preferred rate just for being an existing customer. They're big, established, and accessible just about anywhere.

Credit unions, on the other hand, are non-profits owned by their members. This different structure means they often pass the savings back to you in the form of lower interest rates and fewer fees. The service can also feel a bit more personal and flexible, which many people appreciate.

My best advice? Apply at both your bank and a local credit union. This lets you compare actual, concrete offers. You can use one offer to negotiate with the other, ensuring you squeeze every bit of value out of the deal and land the best loan possible.

Whichever you choose, preparation is your superpower. A strong credit history and a decent down payment will make these traditional lenders your best bet for stable, reliable, and competitive RV financing.

Once you venture beyond the traditional walls of banks and credit unions, you'll find a whole world of other financing options. This is where specialized lenders come into play—from the finance office at your local RV dealership to nimble online platforms. Each has its own flavor of convenience, speed, and loan terms, giving you more paths to explore on your way to hitting the road.

Dealer financing is often the path of least resistance. You find the perfect rig, and you can hammer out the loan paperwork right then and there. It’s a true “one-stop shop” experience, which is a huge plus, especially if this is your first RV purchase. The trade-off for that convenience? You might find that the interest rates are a tad higher than what you could secure if you shopped around on your own first.

Then you have online lenders. These digital-first companies are built for speed and competition. You can often get a loan decision in minutes, and many platforms will serve up multiple offers from their network of lending partners. The whole process is incredibly efficient, but it does lack the personal touch of sitting across a desk from a loan officer.

Think of these alternative RV financing options as different tools for the same job. Dealer financing essentially makes the dealership a middleman. They have relationships with a network of lenders and will handle the application process for you. This definitely simplifies things, but it can also mean you don't get a full view of every loan product out there.

Online lenders, on the other hand, give you direct access to financing. Their websites and apps are typically designed to make comparing rates and terms a breeze. That transparency is a major win, letting you make a smart decision right from your couch. It really comes down to weighing the sheer convenience of a dealership against the competitive marketplace you'll find online.

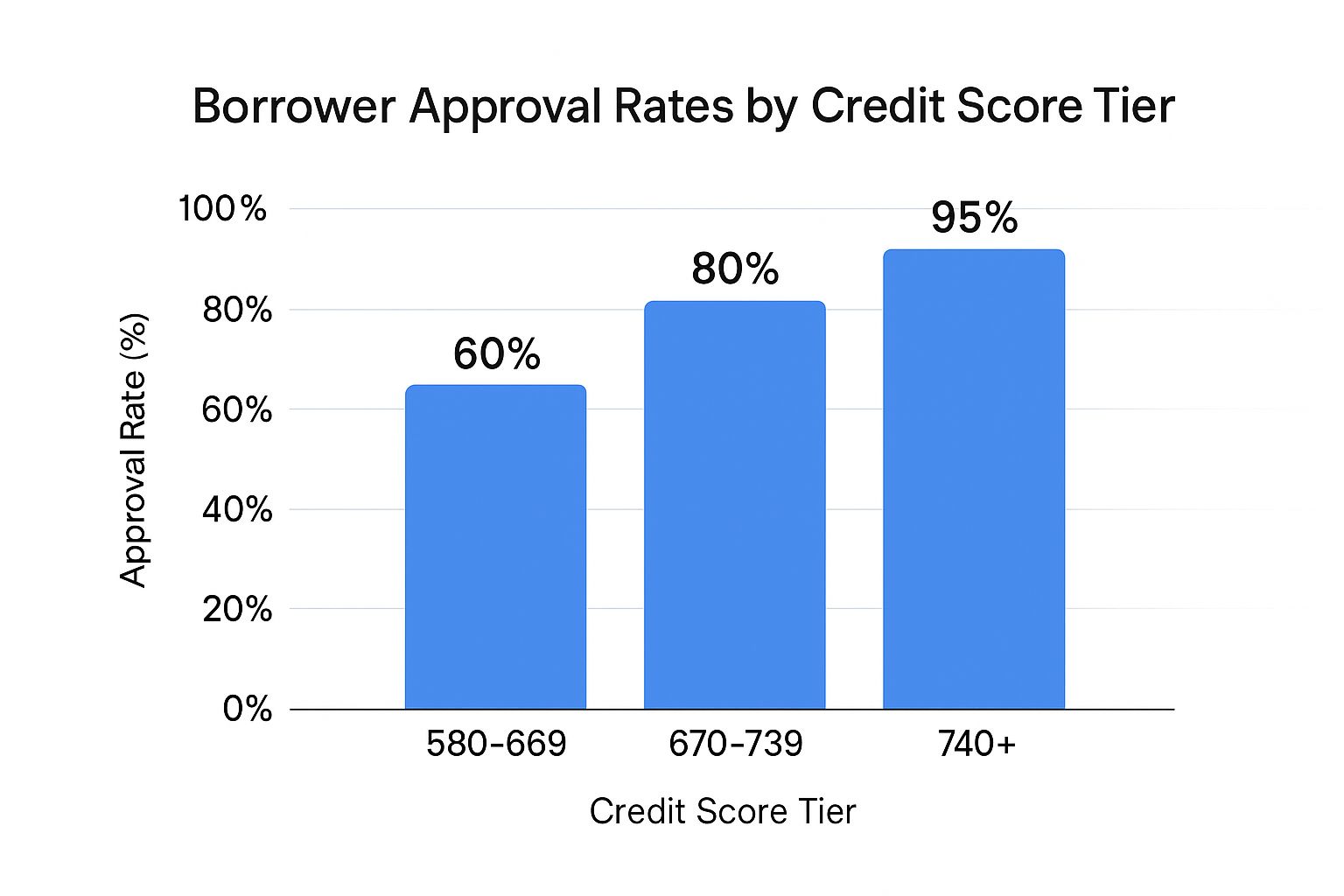

No matter which lender you choose, a strong credit score is your golden ticket. Lenders see a high score as proof that you're a reliable borrower, which dramatically boosts your approval odds and helps you lock in a much lower interest rate.

Your credit history is the foundation of any loan application. As the infographic below clearly shows, there's a direct line connecting higher credit scores to better approval rates.

The data speaks for itself. If you have excellent credit (740+), your chances of getting approved are almost a sure thing. This is exactly why it's so important to know your score before you even start looking.

For a big recreational purchase like an RV, lenders are laser-focused on financing borrowers they see as low-risk. The numbers back this up: prime borrowers with credit scores over 720 made up a whopping 54.83% of all recent RV loan originations. It's a clear signal of who lenders feel most comfortable with. You can dive deeper into the RV loan origination data and trends to get a better sense of the market.

To help you sort through your options, the table below provides a quick snapshot of what to expect from different types of lenders.

This table compares key features of different RV financing sources to help you decide which is best for your situation.

| Financing Option |

Typical Interest Rate Range |

Common Loan Term |

Best For |

| Dealer Financing |

Moderate to High |

10-20 Years |

Buyers who want maximum convenience and on-the-spot financing. |

| Online Lenders |

Competitive to Moderate |

10-15 Years |

Shoppers looking to quickly compare multiple loan offers online. |

| Specialized RV Lenders |

Competitive |

15-20 Years |

Borrowers seeking expert guidance and terms tailored specifically for RVs. |

| Credit Unions |

Low to Competitive |

10-15 Years |

Members who value personal service and are hunting for the lowest rates. |

So, what’s the best choice? It really boils down to what you value most. Are you prioritizing speed, personal service, or the absolute lowest interest rate you can find? By taking the time to explore all these avenues, you put yourself in the best possible position to land the financing that gets your adventure started right.

When you start looking for an RV loan, there's one number that matters more than any other: your credit score. Think of it as your financial report card. Lenders use it as a quick snapshot to judge how reliable you are with money. A high score signals that you have a solid history of paying your bills on time, making you a much safer bet.

This single number has a massive impact on every part of your loan offer. It directly influences your interest rate, how long you have to pay it back, and even the maximum amount you'll be approved for. A great score can open the door to the best rates and most flexible terms, while a lower score almost guarantees a more expensive loan.

And we're not talking about a small difference here. Even a tiny shift in your interest rate can easily add up to thousands of dollars over the 10 to 20-year life of a typical RV loan.

Let’s get specific to see how this plays out in the real world. Say you’re looking to finance a $75,000 RV over 15 years. Here’s a breakdown of how different credit scores could dramatically alter your deal:

- Excellent Credit (760+): You could land an interest rate around 6%. This puts your monthly payment at about $658, and you’d pay roughly $43,400 in total interest over the life of the loan.

- Fair Credit (650-699): Your rate might jump to 10%. Suddenly, your monthly payment is $806, and the total interest skyrockets to over $70,000.

- Poor Credit (Below 620): With a rate closer to 15%, your payment would be a steep $1,023 per month. The total interest? A staggering $109,000—far more than the original price of the RV.

As you can see, a strong credit profile doesn't just save you a few bucks each month. It can literally save you tens of thousands of dollars over the long haul.

Your credit score is the key that unlocks better financial doors. Polishing it before you apply is the single most effective way to lower the long-term cost of your RV adventure, giving you more financial freedom on the road.

If your score isn't quite where you want it to be, don't sweat it. There are concrete steps you can take to give it a tune-up before you ever fill out a loan application.

First things first, pull your full credit reports from all three major bureaus—Equifax, Experian, and TransUnion. Comb through them carefully, looking for any errors or inaccuracies. A wrong account or a misreported late payment could be dragging you down. Disputing these mistakes is often the fastest way to see a nice bump in your score.

Next, turn your attention to your credit cards. Paying down high balances is a game-changer because it lowers your credit utilization ratio—that's the percentage of available credit you're currently using. Lenders love to see this ratio below 30%, as it shows you aren't financially overextended.

For those with lower scores, it’s all about setting realistic expectations. Some lenders will finance RVs for people with scores as low as 550, but be prepared for very high interest rates. While the best rates can be as low as 5.99%, riskier profiles might see rates climbing toward 19.95%. You can get a better sense of the current landscape of RV loan rates and how they track with credit scores. Even if your score is on the lower end, you can still strengthen your application by demonstrating a stable income and making a larger down payment.

Walking into the RV loan application process can feel a little daunting, but it doesn't have to be. If you break it down into a simple checklist, you’ll find it’s much more approachable.

The real secret is doing your homework before you even talk to a lender. A little preparation now can save you a ton of headaches—and money—down the road. Taking these steps shows any bank, credit union, or dealer that you’re a serious, low-risk applicant.

Your first and most important move is to build a realistic budget. This isn't just about the sticker price of the RV; it's about figuring out the total cost of ownership. A lot of first-time buyers get blindsided by the little expenses that can easily add hundreds of dollars to their monthly budget.

Before you fill out a single form, sit down and map out all the costs that come with owning a rig. A detailed budget proves to lenders that you’ve really thought this through.

- Insurance: This can swing wildly depending on the RV model, its value, and your driving history. Get a few quotes early on.

- Maintenance: You'll need to set aside money for the essentials—think oil changes, tire rotations, and checking the roof seals.

- Storage: Don't have a spot at home? Monthly storage fees can be a hefty, recurring cost you need to account for.

- Fuel: Let's be honest, RVs are thirsty. This will likely become a major line item in your travel budget.

Once your budget is locked in, it's time to gather your paperwork. Lenders will want to see proof of your income (like pay stubs or tax returns), your ID, and a clear picture of your current debts and assets. Keeping everything in one place will make the actual application a breeze.

Here’s a pro tip: Get pre-approved by a few different lenders before you set foot on a dealership lot. This gives you a hard budget to stick to and a massive bargaining chip when it’s time to negotiate the price.

Finally, try to sidestep a few common mistakes that catch even the most prepared buyers off guard. The biggest one? Only getting a single loan quote, especially if it’s just from the dealer. If you don't shop around, you'll never know if you're leaving a better deal on the table.

And always, always read the fine print before you sign anything. Keep an eye out for sneaky terms like prepayment penalties that could cost you later. By following these steps and staying organized, you can turn what feels like a stressful chore into a confident first step toward your next big adventure.

As you start digging into financing options, a few key questions always seem to pop up. Think of this as the FAQ section—getting these sorted out now will give you the confidence you need when it’s time to make a deal.

Let's clear up some of the most common uncertainties people have before signing on the dotted line.

One of the first things people notice is that RV loans aren't like your typical car loan. While you might finance a car for five or six years, RV loans stretch out much longer, closer to what you’d see with a home mortgage.

Most RV loan terms fall somewhere in the 10 to 15-year range. If you’re eyeing a big Class A motorhome or a high-end fifth wheel, it’s not uncommon to see lenders offer terms as long as 20 years.

The upside is a lower monthly payment that’s easier on your budget. The downside? A longer loan means you'll pay quite a bit more in total interest over the years. It's a classic trade-off you'll need to weigh.

Absolutely. Financing a used RV is very common, but lenders approach it a little differently than a brand-new model. To protect themselves, they often have rules about the age and mileage of the RV they’re willing to finance.

You’ll also probably notice that the loan terms are a bit shorter and the interest rates a touch higher for a used rig. This is simply because an older vehicle carries a bit more risk of needing repairs down the road.

One of the biggest financial questions is whether you can write off the interest on your RV loan. The answer is a potential "yes," and it could save you a good chunk of money come tax time.

For the interest to be tax-deductible, your RV has to qualify as a second home. This means it needs to have the essentials: a place to sleep, a kitchen area, and a toilet. If it ticks those boxes, the IRS may view it just like a second mortgage.

But—and this is a big but—tax laws are notoriously tricky. Before you bank on that deduction, talk to a tax professional who can look at your specific situation and give you the right advice.

Ready to turn that RV dream into a reality? At Searchshop, we simplify the whole process. You can browse thousands of RVs, compare your options, and even get pre-qualified for financing all in one place. Your next adventure is waiting. Start exploring our huge RV selection today.