So, you’ve got the boating bug. Before you get swept away by visions of open water and sunny days, let’s talk about the most important first step: getting your financial ducks in a row. Seriously, a solid budget is the bedrock of a happy boat or RV ownership experience.

This isn’t about killing the fun; it’s about making sure your new recreational vehicle remains a joy, not a financial headache. Nailing down your numbers before you ever talk to a dealer puts you in the driver’s seat.

The most exciting part is picking out the boat or RV, I get it. But the real work—the work that makes everything else possible—happens with a calculator and a bit of honest planning.

Think of it this way: having a firm budget empowers you. When you know exactly what you can comfortably afford, you can walk into a dealership with confidence, negotiate from a place of strength, and sidestep the pressure to overspend.

When you walk into a lender's office, a healthy down payment speaks volumes. It shows them you're serious and financially prepared. Most lenders will want to see at least 10% to 20% of the vehicle's price, but pushing for the higher end of that range is always a smart move.

Why? A bigger down payment means you borrow less. That simple fact leads to a lower monthly payment and, more importantly, less money paid in interest over the life of the loan. On a $50,000 boat, putting down 20% ($10,000) instead of 10% ($5,000) can literally save you thousands and make your monthly budget much more comfortable.

Pro Tip: From my experience, hitting that 20% down payment mark is often the magic number for both boat and RV loans. It can unlock better interest rates and more flexible terms because it signals to lenders that you're a lower-risk borrower.

Your credit score is the first thing a lender looks at to gauge your financial reliability. Before you even start browsing boat or RV listings, you need to know exactly where you stand. Pull your reports from all three major bureaus—Equifax, Experian, and TransUnion.

Give them a thorough review. You might find errors that are unfairly dragging down your score, and getting those corrected can make a huge difference. Generally, marine and RV lenders get excited when they see a score of 700 or higher, as that’s usually the threshold for their best rates. If you’re not there yet, it doesn’t mean you can’t get a loan, but you should probably expect a higher interest rate.

The sticker price on the side of the boat or RV? That’s just the cover charge. The real cost of ownership is a collection of ongoing expenses that can catch new owners by surprise. Budgeting for these from day one is non-negotiable.

To help you get a clear picture, here’s a breakdown of what you should anticipate paying every year for a boat.

A realistic breakdown of the recurring annual costs to help you build a comprehensive and sustainable boat budget.

| Expense Category |

Estimated Annual Cost (as % of Boat Value) |

| Insurance |

1.5% - 3% |

| Maintenance & Repairs |

5% - 10% |

| Storage / Moorage |

2% - 10% |

| Fuel |

Varies widely |

| Taxes & Registration |

1% - 2% |

Don't let these numbers scare you; let them prepare you. Forgetting to budget for insurance, a slip fee, or routine maintenance is the fastest way to turn your dream into a source of stress. The old rule of thumb is to set aside about 10% of the boat's value for annual upkeep, and it's a solid guideline to follow. For an RV, these costs include storage, insurance, maintenance, fuel, and campground fees.

It's also worth noting the bigger picture. The economy definitely affects the recreational market. With factors like inflation and shifting interest rates, lenders are being more careful. As the latest report from the National Marine Manufacturers Association shows, buyers are being more cautious, which means a well-prepared application and a solid budget are more crucial than ever to secure a good loan.

Alright, you've nailed down your budget. Now comes the part that feels daunting to many: finding the actual cash.

The world of marine and RV financing is surprisingly deep, and understanding your options is the key to getting a deal that feels right for you, not just for the bank. It's definitely not a one-size-fits-all game. The best loan really depends on the vehicle you want, your financial situation, and what you're looking for long-term.

Taking a bit of time to explore the landscape can genuinely save you thousands over the life of your loan. Let's break it down.

First thing's first, you'll run into two main types of loans.

The most common path by far is a secured loan. Think of it just like a car loan—the boat or RV itself acts as the collateral. This means if you stop making payments, the lender can repossess the vehicle. Because this setup is much safer for the lender, they're willing to offer you better deals. We're talking lower interest rates and much longer repayment terms, often stretching out 10 to 20 years.

Then you have unsecured personal loans. These don't require any collateral; a lender gives you the money based purely on your credit score and income. While the simplicity is tempting, that higher risk for the lender translates directly to higher interest rates and shorter terms for you. An unsecured loan might work for a small, inexpensive jon boat or a pop-up camper, but for most serious boat or RV purchases, the secured loan is the smarter financial move.

You’ve got a few different doors to knock on when looking for a lender. Each has its pros and cons, so it’s smart to check out at least a couple before you commit.

-

Dealership Financing: This is hands-down the most convenient route. You find the boat or RV and sort out the financing all in one go. Dealers work with a network of lenders—many who focus specifically on recreational vehicles—and can usually line up a few offers for you on the spot. It’s a great option if you’re buying new and want a quick, streamlined process.

-

Specialized Marine Lenders: These folks are the pros. They live and breathe boat loans. They get the nuances, from arranging marine surveys for used boats to handling title work for a private sale. Because of their expertise, they can often be more flexible and offer really competitive rates, especially if you're looking at a larger vessel or something unique. The same goes for specialized RV lenders.

-

Banks and Credit Unions: Don't forget your own bank or local credit union. If you have a good, long-standing history with them, they might offer you very favorable terms as a loyal customer. Credit unions, in particular, are famous for their member-first approach and often have some of the best interest rates you’ll find anywhere.

Choosing the right lender isn't just about chasing the lowest possible rate. A marine specialist might cost a fraction of a percent more but save you a world of headaches on a complex private sale. On the flip side, a dealership might have a promotional rate that simply can't be beaten.

Let’s look at how this plays out for two very different boat buyers.

Scenario A: The New Wake Boat Buyer

You’ve got your eye on a shiny new $90,000 wake boat. You're trading in your old runabout and want the whole thing to be as painless as possible.

In this situation, dealership financing is probably your best move. The dealer can wrap your trade-in, down payment, and new loan into a single, clean transaction. Plus, they often have access to manufacturer-backed financing with killer promotional rates that a standard bank just can’t offer.

Scenario B: The Used Sailboat Seeker

Now, let's say you're buying a 15-year-old, $45,000 sailboat from a private seller a few states over. A traditional bank might get nervous about financing an older boat, especially when it's a private sale.

This is where a specialized marine lender becomes your best friend. They're completely comfortable with private-party sales. They know a thorough marine survey is non-negotiable and can manage the escrow and title transfer to protect both you and the seller. Their expertise turns a potentially messy purchase into a smooth, secure process.

So, you've zeroed in on the right type of lender and you're ready to go for it. A strong loan application is much more than just filling out forms—it’s about presenting a clear, compelling story about your financial stability.

Think of it as your personal financial resume. The goal is to show the lender you're a reliable, low-risk borrower. Get this right, and you'll not only speed up approval but also lock in the best possible terms. The more prepared you are on the front end, the smoother the whole process will be.

To make a sound decision, lenders need to see the full picture of your finances. This goes beyond simply stating your income. Having all your paperwork ready from the get-go saves you from the frustrating back-and-forth that can stall an application.

Before you even start filling out forms, get these essential documents together:

- Proof of Income: This usually means your last two pay stubs. If you’re self-employed, plan on providing your last two years of tax returns to show a consistent earnings history.

- Tax Returns: Speaking of which, most lenders will want to see your complete tax returns for the past two years to verify everything.

- Bank Statements: Have the last two or three months of your checking and savings account statements ready to go. This gives them a clear look at your cash flow and assets.

- Personal Financial Statement: This is a simple snapshot of everything you own (assets) and everything you owe (liabilities). It’s crucial to be completely honest and accurate here.

Organizing these items ahead of time sends a strong signal to the lender that you're serious and well-prepared, which really sets a positive tone for the whole process.

When a loan officer digs into your file, they're laser-focused on two key numbers that tell them how much risk they're taking on: your credit history and your debt-to-income ratio.

Your credit report is the story of how you've handled debt in the past. They're looking for a consistent history of on-time payments. A single late payment from five years ago isn't a deal-breaker, but one from last month is a much bigger red flag. A clean record is always your best bet.

The other major piece of the puzzle is your Debt-to-Income (DTI) ratio. It’s a straightforward calculation: your total monthly debt payments divided by your gross monthly income. Lenders really like to see a DTI of 40% or less, and that includes the new boat or RV payment you're applying for.

I see people make this mistake all the time: they apply for a major loan while carrying small, nagging credit card balances. Even if they're minor, several small debts can clutter your credit report and nudge your DTI up. Paying off these "nuisance" balances a month or two before you apply cleans up your profile and makes you look like a much stronger candidate.

The great news for anyone in the market right now is that conditions are pretty favorable. Boat loan interest rates have recently become much more affordable, with some leading marketplaces offering rates as low as 6.49%. That's a huge drop that makes ownership more accessible and keeps those monthly payments down. You can get more details on how these lower rates are impacting the market on Boat Trader.

Knowing this helps you time your purchase. Applying when rates are low gives you an immediate advantage.

It's also a smart move to get pre-approved before you start seriously negotiating on a boat or RV. Walking in with a pre-approval letter is like having cash in your pocket. It shows sellers you're a qualified buyer ready to pull the trigger, giving you some serious leverage. This one step transforms you from a tire-kicker into a serious contender.

Getting that pre-approval letter feels fantastic, but hold the celebration. You're not at the finish line yet—you're just getting into the final turn. Securing an approval is one thing; locking in the best possible deal is the real win. This is where you shift from being a loan applicant to a savvy negotiator.

Now's the time to put on your glasses and scrutinize every single detail before signing anything. It’s about so much more than just the interest rate. The loan term, sneaky little fees, and potential penalties can completely change the total cost of your new vehicle over the long haul.

If you played your cards right, you might have a few loan offers to choose from. That’s a great spot to be in. The trick is to look beyond the monthly payment and focus on the total cost of borrowing.

Don't get dazzled by a slightly lower monthly payment that’s attached to a much longer loan term. That's a classic trap that can cost you thousands more in interest. You need to lay out the critical details for each offer to see the full, unvarnished picture. A simple comparison chart often reveals which deal is genuinely better for your wallet.

The single biggest mistake I see buyers make is getting tunnel vision on the interest rate. A loan with a 6.5% rate for 15 years might look better on paper than one with a 7% rate for 12 years, but you could easily end up paying thousands more in total interest on that longer-term loan. Always, always run the numbers.

To make this easier, here's a simple template you can use to compare your offers. Just plug in the numbers from each lender to see a clear, side-by-side breakdown.

| Loan Feature |

Lender A Offer |

Lender B Offer |

Lender C Offer |

| Loan Amount |

| Interest Rate (APR) |

| Loan Term (Months) |

| Monthly Payment |

| Origination/Admin Fees |

| Prepayment Penalty? |

| Total Interest Paid |

| Total Loan Cost |

Once you fill this in, the "Total Loan Cost" row will tell you everything you need to know. It’s the true bottom line.

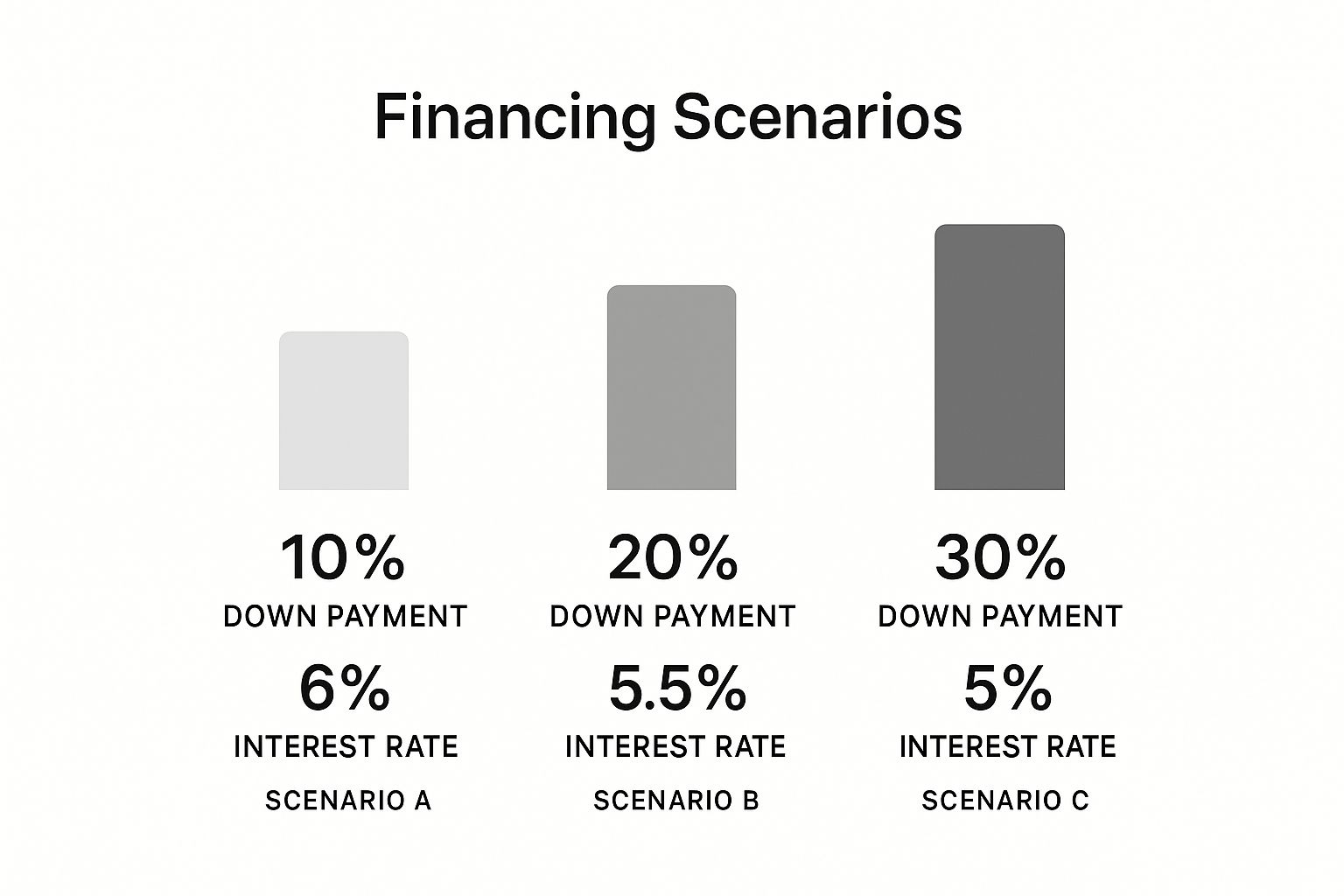

Think of your down payment as your most powerful negotiating chip. The more money you put down, the less risk the lender takes on. That often makes them much more willing to give you a better interest rate. If you have the cash, bumping up your down payment can lead to some serious long-term savings.

This infographic shows just how much of a difference a bigger down payment can make.

As you can see, a larger chunk of cash upfront doesn't just lower your loan amount—it can unlock a better rate, saving you a bundle over the life of the loan.

I'm going to be blunt: if you are buying a used boat, you absolutely must get a professional marine survey and a sea trial before you sign the final papers. This isn’t a friendly suggestion; it’s a non-negotiable step to protect yourself. A marine surveyor is essentially a home inspector for boats, and they will give you an exhaustive report on everything from the hull's integrity to the engine's health. For an RV, a certified RV inspection serves the same critical purpose, checking everything from the chassis to the appliances.

The survey or inspection report is your ultimate negotiation tool. If the professional finds problems—even seemingly minor things like worn-out pumps or dated electronics—you take that report right back to the seller. You can then negotiate for a lower price to cover the repairs or insist that the seller fixes everything before the deal is done.

This isn't just for small boats, either. Even in the high-end market, buyers are doing their homework. The superyacht segment, for example, saw a 44% surge in sales recently, yet the average time a yacht sat on the market actually went up. This tells us that even big-money buyers are being more deliberate and thorough. You can read more about trends in the yacht market and see how deliberate buyers are.

Okay, you’ve hammered out the final price and financing. It's time to close. This is where you sign the mountain of legal documents. It can feel intimidating, but knowing what to look for will make it a smooth process.

You’ll be reviewing and signing a few key documents:

- The Loan Agreement: This is the big one. It spells out every term of your financing—the interest rate, the loan term, your payment schedule. Read. Every. Single. Word.

- The Bill of Sale: This is the document that legally transfers the boat or RV from the seller to you. Double-check that all the details, especially the Hull Identification Number (HIN) or Vehicle Identification Number (VIN), are perfect.

- Title and Registration Paperwork: These are the forms to get the vehicle officially titled and registered in your name with the proper authorities.

- Security Agreement: For a secured loan, this document officially lists the boat or RV as collateral.

Don’t be shy about asking questions. If you see a fee you don’t recognize or a clause that seems confusing, speak up. This is your final chance to make sure everything is exactly as you agreed. Once the ink is dry, the keys are in your hand, and you’re ready to hit the water or the open road.

A standard marine or RV loan is the go-to for most people, and for good reason. It’s a well-worn path. But what if it’s not the best path for you? Sometimes, your credit history, the specific vehicle you want, or just a desire for more financial breathing room means you need to think outside the box.

Don't worry, you're not out of options. In fact, exploring some alternative financing routes can open up possibilities you might not have considered. They often require a bit more legwork and careful planning, but for the right person and the right situation, they can be the perfect key to unlocking your dream of owning a boat or RV.

If you're a homeowner, you might be sitting on one of the most effective financing tools available: a Home Equity Line of Credit (HELOC). Think of it as a flexible credit line secured by the equity you’ve built up in your house. Because your property is the collateral, lenders see it as a very low-risk loan, which means you can often score a much lower interest rate than you'd get with an unsecured personal loan or even some recreational loans.

The biggest draw here is the savings. A lower rate translates directly to a smaller monthly payment and less money paid in interest over the long haul. Plus, a HELOC gives you flexibility. You draw funds as you need them, which is perfect if you’re planning on buying the boat or RV and then tackling a few upgrades or refitting projects right away.

But—and this is a big one—you have to go into this with your eyes wide open. You are leveraging your home. If life throws you a curveball and you can't make the payments, the lender has the right to foreclose. This strategy really only makes sense if your financial footing is rock-solid and you're disciplined enough to not overextend yourself.

You might be surprised to learn that sometimes the best lender is the person selling you the vehicle. This is called seller financing (or an "owner-carry" deal), and it’s most common in private sales. It can be a lifesaver if you're having trouble getting a thumbs-up from a traditional bank.

This kind of arrangement can be a true win-win. The seller gets their full asking price while also earning some interest, and you get your boat or RV without jumping through all the hoops at the bank. The best part? The terms are completely negotiable. You and the seller work out the interest rate, down payment, and payment schedule together.

A word of caution: this is absolutely not the time for a handshake agreement. Everything needs to be buttoned up in a legally binding contract, preferably drafted by an attorney specializing in these types of transactions. That document should spell out everything in plain English:

- The total price and the exact down payment.

- The agreed-upon interest rate and payment schedule.

- Clear consequences for late or missed payments.

- Who officially holds the title until the final payment is made.

Crucial Insight: Whenever I advise clients on seller financing, I insist they use a third-party escrow service. The service acts as a neutral middleman, holding the vehicle's title and managing the payment process. Once you make that last payment, they release the title to you. It’s the single best way to protect both you and the seller from headaches down the road.

Feeling a little sticker shock from the total cost of ownership? You don't have to carry the entire load yourself. Boat and RV partnerships or fractional ownership are gaining a lot of traction as smart, affordable ways to get on the water or on the road. Instead of financing 100% of a vehicle, you’re just financing your share.

A simple partnership could mean going in with a friend or family member. You split the purchase, the down payment, and all the recurring costs—insurance, storage, maintenance, you name it. It dramatically lowers the barrier to entry. The secret to a happy partnership, though, is a detailed agreement written before any money changes hands. It must cover who uses the vehicle when, how costs are divided, and what happens if one of you wants to sell their share.

Fractional ownership is a more structured version of this, typically run by a professional management company. You buy a share in a specific boat, RV, or even a fleet, which gives you a set number of days of use each year. The company handles all the dirty work—maintenance, cleaning, scheduling, and storage. It's a fantastic, hassle-free way to enjoy the lifestyle for a fraction of what it would cost to go it alone.

Stepping into the world of boat and RV financing can feel a little confusing at first. Even if you've bought a vehicle before, the market changes, and new questions always pop up. Let's tackle some of the most common things people ask, so you can move forward feeling completely confident.

Think of this as your quick-reference guide for all those little details that can otherwise become big headaches. Getting these sorted out now will save you a ton of time and stress down the road.

There's no single magic number, but most marine and RV lenders really start to take notice when they see a credit score of 700 or higher. If you’re in that range, you’ll likely see their best interest rates and most flexible loan terms.

Don't panic if your score is in the mid-to-high 600s, though. You aren’t automatically out of the running. You can often still get approved, but the lender will probably want a larger down payment or offer a slightly higher interest rate to balance out their risk. They're looking at your whole financial picture, so things like a steady job history and a low debt-to-income ratio can really bolster your application, even with a less-than-perfect score.

This is one of the biggest differences between buying a boat or RV and buying a car. These recreational loans can stretch out for a long time, often anywhere from 10 to 20 years. The size of the loan is really what dictates the term. You might see a 5 to 10-year term for a smaller loan on a used pontoon or travel trailer, but it's common for a big loan on a new cruiser or Class A motorhome to be financed over 20 years.

A longer term gives you a lower monthly payment, which is great for your budget. The trade-off, of course, is that you'll pay a lot more in total interest over the life of the loan. It’s all about finding that sweet spot between a payment you're comfortable with and the total cost of the vehicle.

Absolutely. While some big, traditional banks might shy away from private-party sales, most specialized marine or RV lenders handle them all the time. It’s a normal part of their business.

The process is pretty similar to buying from a dealership, but there are a few extra steps to protect everyone involved. The lender will almost certainly require a professional marine survey (for a boat) or a certified inspection (for an RV) to check the vehicle's condition and a detailed title search to make sure there are no hidden liens on it.

From my experience, using an escrow service for a private sale is non-negotiable. The lender will often set this up. A neutral third party holds your money and the vehicle's title until everything is finalized. It’s the best way to ensure the funds and the title transfer safely, protecting both you and the seller.

You should plan on putting down between 10% and 20% of the vehicle's purchase price. While you might be able to get by with 10%, aiming for 20% is always the smarter financial move.

Putting more money down is a powerful signal to lenders. It lowers your loan-to-value ratio, which reduces their risk and often convinces them to give you a better interest rate. Plus, a bigger down payment means you're borrowing less money, which leads to a smaller monthly payment and saves you a bundle in interest over time. It's the best way to start your life as a boat or RV ow